By: Benjamin Katzeff Silberstein

Prices for rice have fallen in North Korea. Daily NK, which tracks prices of rice and foreign currency in three North Korean cities, reported in the beginning of this week that rice prices have fallen thanks to continued development of the market economy and a steady flow of goods to and from China. This has happened despite expectations that the sanctions that the UN passed one year ago would cause inflation.

In theory, the sanctions were supposed to curb trade with China because they targeted North Korea’s crucial minerals trade. In practice, a steady stream of news from the border suggests that trade has continued, albeit with periodic squeezes, following a familiar pattern of China’s sanctions implementation waxing and waning.

This makes a lot of sense. A better functioning and more efficient market should logically lead to lower prices, as should increased trade with China, given the increase in supply. But neither of these two factors explains the timing. There are several other elements to take into consideration when analyzing price changes in North Korea. I am not making any certain claims here about the relatively drastic shift in prices, but rather, pointing to a few factors that may have contributed.

First, one must ask: how big is the drop? The short answer is: pretty big, but not unprecedented. The following graph shows the last and first price observations in the Daily NK market prices database for every year since 2010–2011. (I’ve excluded 2009–2010 because of the distortions that the 2009 currency reform creates in the data.) It shows that a similar price drop happened between 2011 and 2012 as well.

Graph 1: rice prices in North Korea, last and first year observations. Graph by NKeconwatch.com. Data from Daily NK.

This latest price point, however, is not a historic low-point. We’ll see if prices continue to drop over the weeks, but as of now, there are fairly near time points when prices have been lower, such as April 2014 (see graph further down).

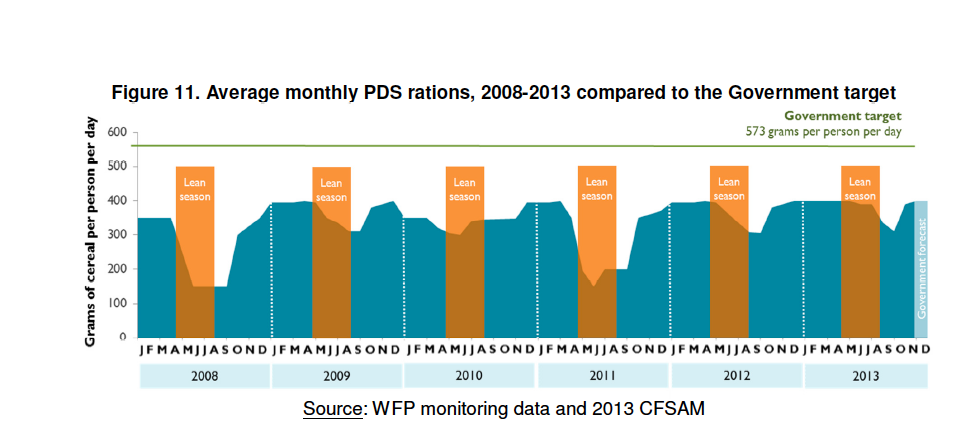

Prices are seasonal to a degree. Though the market system and the public distribution system (PDS) obviously function under very different mechanisms, the following graph from the World Food Program’s 2013 food and crop assessment (the latest exhaustive one they published, to my knowledge) underscores the point that supply varies depending as the harvest draws farther and closer, and suggests that overall supply tends to be particularly good in December and January in other years as well:

Figure copied from World Food Program Food and Crop Assessment in the DPRK, November 2013, showing seasonal variations in government grain distribution.

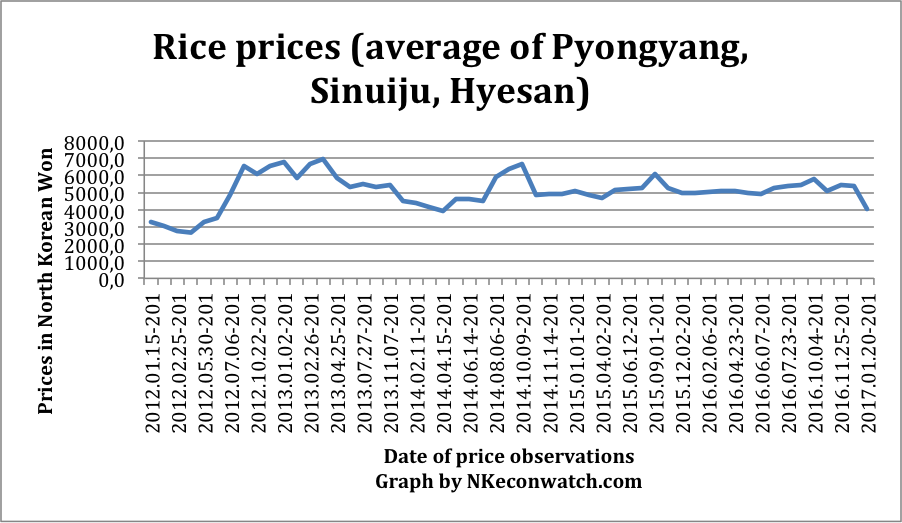

Overall, the story under Kim Jong-un’s tenure seems to be one of price stability. Since around the spring of 2014, prices have moved in a fairly delineated fashion (as visible in the right half of this graph):

Rice prices, average of three cities, 2012–2017. Data from Daily NK, graph by NKEconwatch.com.

Second, though it would be intuitively easy to conclude that the drop in prices was caused by better functioning market mechanisms and agricultural management changes, this doesn’t seem to be the whole story. Again, such changes are crucial and may well have played a large role in the greater price stability of the past few years. But they would not explain this sudden shift.

Instead, the story seems to partially be the opposite, one of government action. A few days ago, Voice of America reported that PDS distributions in January of this year have, according to a World Food Program official, gone up by around ten percent as compared to the same period last year. Both in September and November, the North Korean government imported significantly larger quantities of rice than usual. These imports presumably go out through state channels rather than the private markets.

So while it’s impossible to isolate different effects from one another, it looks like the state can still have a significant impact on the food economy, even with the strong and continuously evolving market sector. This impact seems particularly likely this time around, given the sudden drop in prices. Only time will tell whether drop continues, or if prices continue to bounce within the limits of the past few years.